Gone are the days when the pharmacy benefit defined the lay of the land for an insured member. While the vast majority of prescriptions are still purchased using insurance, pharmacy consumers increasingly look for the lowest-cost options, whether found in their prescription benefit or somewhere else.[i]

Discount cards may have started this trend, but a growing number of direct purchase options are driving it today. Various direct options bypass traditional insurance and intermediaries, yet only for certain medications. Within the covered benefit, various patient assistance programs also contribute to an expanding plate of affordability solutions.

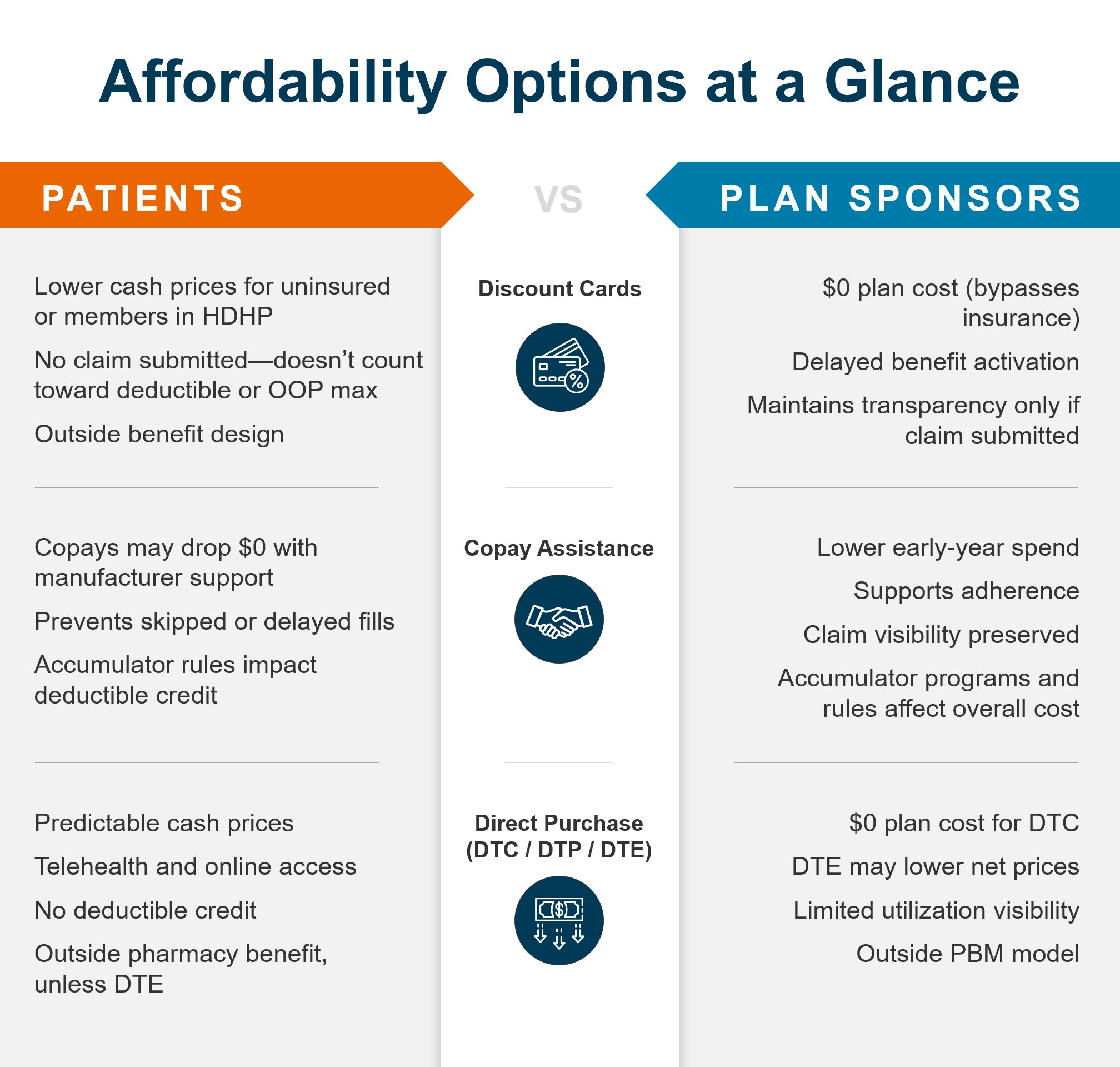

Here’s a breakdown of the impact each can have on both patient out-of-pocket (OOP) costs and plan sponsor pharmacy spend.

1. Discount Cards

Discount cards reduce the cash price patients pay at the pharmacy, often making medications more affordable—especially for members with high-deductible plans, or patients without insurance. Some major for-profit discount card providers advertise up to 80% savings over retail pharmacy cash prices.[ii]

For patients:

Discount cards can broaden access for some patients by reducing cost barriers even when insurance is not used. This may help some patients who might otherwise skip or delay needed treatment.

For plan sponsors:

Discount-card transactions bypass insurance, meaning there is no cost incurred by the plan. Whatever the member spends doesn’t count toward their deductible or out-of-pocket maximum—potentially delaying when insurance benefits fully activate. (Note: Some plan sponsors may allow members to submit cash pay purchases and apply toward deductibles.)

However, because the claim never passes through the pharmacy benefit, plan sponsors typically lose the data into patient utilization patterns, disease management opportunities, and potential safety monitoring.

2.Biopharma Copay Assistance

Copay assistance comes in a variety of names and forms, like patient assistance programs, copay cards/coupons, and manufacturer coupons. Collectively, these are often referred to as affordability programs.

For patients:

These programs reduce the amount an employee pays at the pharmacy. For some medications, this can turn a several-hundred-dollar copay into a much smaller payment, even $0. For some patients, it can mean the difference between filling a needed prescription and skipping or delaying treatment due to OOP cost.

For plan sponsors:

Self-insured employer plans often pay less when copay assistance is used because the manufacturer’s coupon covers some or all the patient’s cost share, reducing what the plan must pay for the medication during early fills.

Accumulator considerations: With a copay accumulator, the coupon reduces only the member’s payment—not their deductible or out-of-pocket maximum—so the plan benefits by not accelerating the patient toward full plan coverage later in the benefit year.

If a plan does not use a copay accumulator or maximizer, a member may reach their deductible and out-of-pocket cap faster. After that, the plan pays a larger share of costs for the remainder of the year, potentially raising employer drug spending.

3. Direct (to Consumer/Patient or Employer)

Direct-to-patient or -consumer (DTP or DTC) distribution models involve drug manufacturers or vendors making a variety of medications available directly to patients. In direct-to-employer (DTE) models, self-insured employers contract through program administrators for direct access to a manufacturer’s specific drug at a fixed price, subject to cost-sharing and plan design.

Direct purchase options may involve consumer marketing, telehealth evaluation, and cash price pharmacies, or digital platforms for direct purchases with approved prescriptions. Generally, these avenues operate outside the traditional pharmacy benefit.

For patients:

As with discount cards, patients pay a cash price that might be lower than the OOP cost using their pharmacy benefit. DTP prices are not subject to deductibles, co-insurance or other insurance variables, giving patients a clear point of comparison and perhaps fewer surprises at checkout. Similarly, money spent on DTC purchases does not count toward deductibles or OOP maximums

For plan sponsors:

Direct purchase can help a self-insured employer provide members with a potentially lower-cost alternative to benefit pricing or access to medications not covered by the benefit. Whether a member chooses a DTC channel or purchases through a DTE program, the plan cost is zero (unless reimbursement to members is offered). Depending on the arrangement and DTE product, some employers may realize different net pricing outcomes compared to traditional benefit channels

What to Make of the Mix

We’ve outlined the core tenets of these affordability options solely from a cost standpoint. Clinical considerations, data and utilization management control, recent policy developments, and a host of other factors can come into play when evaluating these options at the patient or plan sponsor level.

True to their purpose, discount cards, patient assistance programs and direct purchase options can and often do make medications more affordable for many patients and plans. But not always, and not always for both parties over the long or short term. True value is situational based on patient and plan priorities.

As we have learned over a decade-plus serving millions of RxSS members and hundreds of health plans and plan sponsors, no two clients or populations are the same. It’s up to each to find their sweet spot between affordability and cost control with the right mix of established and emerging options. The right pharmacy solution can connect whatever those fragmented dots may be.

[i] GoodRx Research; “More Americans Than Ever Are Struggling to Afford Their Prescription Medications,” June 27, 2025

[ii] AI Overview; “average savings by using a discount card for prescription drugs,” accessed March 2026